GHAdvisor - Newsletter

Markets & Investing

Where We Are Today

The economy continues to send mixed signals — and if you've been paying attention to the headlines lately, you may think it’s time to panic. Global uncertainty, inflation, and market volatility have many investors feeling uneasy. This is completely understandable. Actual investment portfolio returns do not match the news, however. There has not been a widespread downturn or correction, and history has shown us time and again that disciplined, well-structured investing remains one of the most powerful tools for mitigating risk and building long-term wealth.

Markets have experienced significant volatility, driven by geopolitical events. The war in the middle East has effectively halted a previously strong outlook for growth and the economy. We finished 2025 with a good deal of upward momentum with strong earnings, lower interest rates and low energy prices. 2026 is much more uncertain now.

It is not all bad news as consumer spending remains relatively resilient, the labor market continues to show some strength, and corporate earnings — while uneven across sectors — have largely held up. That said, headwinds remain.

What This Means for Your Portfolio

During times like these, one of the most important things we can do as an investors is resist the urge to make emotional decisions. Selling out of the market during a downturn locks in losses. On the other hand, chasing high returns in speculative investments can expose you to unnecessary risk.

We may continue to have a good deal of volatility, short-term inflation and alarming headlines, but it is important to remember that volatility is a normal and expected part of investing.

This is precisely why having a sound investment strategy — one built around your personal goals, time horizon, and risk tolerance — is so important. Your plan is designed to weather market storms, not react to them.

The Power of Diversification

One of the most effective and time-tested strategies for managing investment risk is diversification. The idea is that when one area of the market struggles, other areas may hold steady or even perform well, helping to cushion the impact on your overall portfolio.

You can see this in the portfolio returns this quarter. Certain areas of the markets are down quite a lot while others are holding steady or are up a bit. The large cap growth sector returned the most in 2023 and 2024 and is currently down the most in 2026. This type of rotation is normal historically.

Diversification Does Not Eliminate Risk — But It Manages It

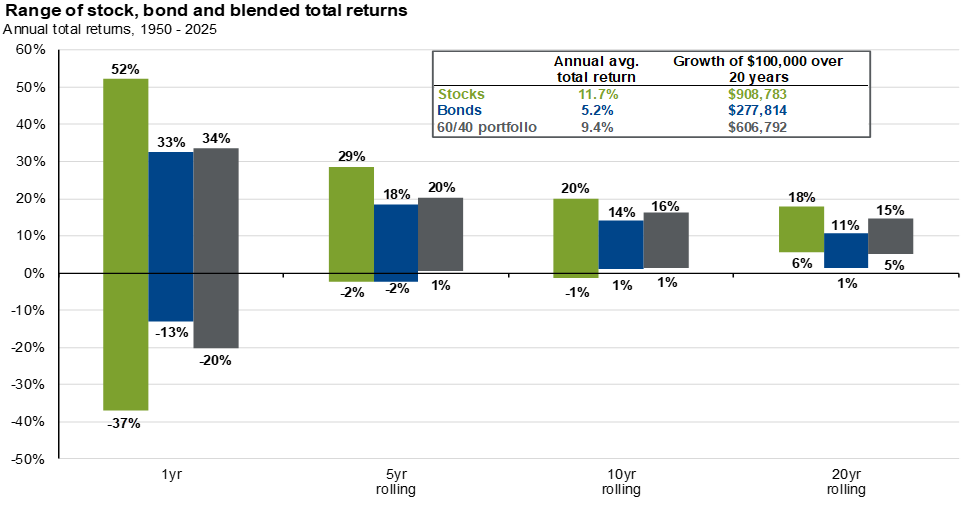

Research consistently shows that investors who maintain diversified portfolios tend to experience less volatility and are better positioned to stay invested through market cycles — which is ultimately what drives long-term results. The chart below illustrates this with a long-term comparison of short to long term returns of stocks, bonds and a blended allocation. Participation in the upside markets while limiting the downside.

Source:

Bloomberg, FactSet, Federal Reserve, Standard & Poor’s, Strategas/Ibbotson, J.P. Morgan Asset Management. Returns shown are based on calendar year returns from 1950 to 2025. Stocks: S&P 500; Bonds: Strategas/Ibbotson for periods pri-or to 1976 and the Bloomberg U.S. Aggregate thereafter. Growth of $100,000 is based on annual average total returns from 1950 to 2025. Guide to the Markets – U.S. Data are as of

Planning

529 Education Accounts – Tax free growth for education - changes

The K-12 withdrawal limit for 529 plans doubled from $10,000 to $20,000 per student starting in 2026, under the One Big Beautiful Bill Act signed July 4, 2025.

529 funds can now also cover vocational training and professional credentialing programs, including CPA exam prep, CDL training, HVAC certification, and cosmetology school.

Under the simplified FAFSA, grandparent-owned 529 distributions no longer count as student income, which removes one of the main reasons families avoided this structure.

The beneficiary definition for 529 plans is broad: siblings, step-siblings, cousins, in-laws, and grandchildren all qualify, which makes unused funds transferable across generations.

Under SECURE Act 2.0, unused 529 funds can roll to the beneficiary's Roth IRA after the account has been open 15 years, capped at $35,000 lifetime and $7,500 per year.

Summer Reading – from Capital Group/American Funds: Capital Ideas TM

“The pleasures of spring are available to everybody and cost nothing.”

George Orwell